Archive

Zombie Arguments Against Fiscal Stimulus

Busy days. I just want to drop a quick note on a piece just published on the Financial Times that is puzzling on many levels. Ruchir Sharma pleads against Joe Biden’s stimulus on the ground that it risks “exacerbating inequality and low productivity growth”. The bulk of the argument is in this paragraph:

Mr Biden captured this elite view perfectly when he said, in announcing his spending plan: “With interest rates at historic lows, we cannot afford inaction.”

This view overlooks the corrosive effects that ever higher deficits and debt have already had on the global economy. These effects, unlike roaring inflation or the dollar’s demise, are not speculative warnings of a future crisis. There is increasing evidence, from the Bank for International Settlements, the OECD and Wall Street that four straight decades of growing government intervention in the economy have led to slowing productivity growth — shrinking the overall pie — and rising wealth inequality.

If one reads the two papers cited by Sharma, they say, in a nutshell, (a) that expansionary monetary policies have deepened income inequality via an increase in asset prices (while for low interest rates and bond prices there is no clear link); (b) that the increasing share of zombie firms drags down the performance of more productive firms thus slowing down overall productivity growth.

So far so good. So where is the problem? Linking these results to excessive debt and deficit, to the “constant stimulus”, is stretched (and I am being kind). A clear case of Zombie Economics.

Let’s start with monetary policy and its impact on inequality (side note: the effect is not so clear-cut). One may see expansionary monetary policies as the consequence of fiscal dominance, excessive deficit and debt that force central banks to finance the government. But, they can also be seen as the consequence of stagnant aggregate demand that is not properly addressed by excessively restrictive fiscal policies, forcing central banks to step in. Many have argued in the past decade that especially in the Eurozone one of the causes of central bank activism was the inertia of fiscal policies. Don’t take my word. Read former ECB President Mario Draghi’s Farewell speech, in October 2019:

Today, we are in a situation where low interest rates are not delivering the same degree of stimulus as in the past, because the rate of return on investment in the economy has fallen. Monetary policy can still achieve its objective, but it can do so faster and with fewer side effects if fiscal policies are aligned with it. This is why, since 2014, the ECB has gradually placed more emphasis on the macroeconomic policy mix in the euro area.

A more active fiscal policy in the euro area would make it possible to adjust our policies more quickly and lead to higher interest rates.

This is as straightforward as a central banker can be: in order to go back to standard monetary policy making, fiscal policy needs to step up its game. Notice that Draghi also hints to another source of problems: the causality does not go from expansionary policies to low interest rates, but the other way round. We have been living in a a long period of secular stagnation, excess savings, low interest rates and chronic demand deficiency which monetary policy expansion can accommodate by keeping its rates close to “the natural” rate, but not address. Once again, fiscal policy should do the job.

Regarding zombie firms, it is unclear, barring the current and very special situation created by the pandemics, why this would prove that stimulus is unwarranted. The paper describes a secular trend whose roots are in insufficient business investment and a drop in potential growth rate (that in turn the authors link to a drop in multi-factor productivity). The debate on the role of fiscal policy in these matters is as old as macroeconomics. In the past ten years, nevertheless, the cursor has moved against the Sharma’s priors and an increasing body of literature points to crowding-in effects: especially when the stock of public capital is too low (as is the case in most advanced countries), an increase of public investment — “constant stimulus”– has a positive impact on private investment and potential growth (see for reference the most recent IMF fiscal monitor and the chapter by EIB economists of the European Public Investment Outlook). Lack of public investment is also widely believed to be one of the factors keeping our economies stuck in secular stagnation.

Fifteen years ago one could have read Sharma’s case against fiscal policy on many (more or less prestigious) outlets. Even then, it would have been easy to argue that it was flawed and fundamentally built on an ideological prior. Today, it seems simply written by somebody living in another galaxy.

My Two Cents on the “Yellow Vests” Movement

In a widely commented televised address President Macron has made a last-minute attempt to stop the “yellow vests” wave, that is investing France and his presidency. After a dramatic (a bit too much to seem sincere, if you ask me) mea culpa on past arrogance, and a promise to “listen to the suffering of the people”, Macron announced a few changes to the French budget law, to sustain the purchasing power of the lower part of the income distribution. The most important and immediate changes are: an increase of minimum wage (more precisely of the “employment subsidy” that is given to most people working at or around minimum wage): the exemption from taxes and social contribution of extra hours (a very popular measure that had been introduced by Nicolas Sarkozy and later abolished by François Hollande); and last but not least, the repeal of the increase of social contributions for retirees, and the confirmation of the freezing (for at least the year 2019) of the “ecological tax” on fuel. Macron also signaled the intention to backtrack on his vertical leadership style (the président jupitérien); he pleaded for renewed role for intermediate bodies (most notably the mayors and local politicians) in putting in place a concerted effort (a “social compact”) to boost growth and social cohesion.

Will Macron’s announcement appease the uprising that inflames France? Most probably not, because they suffer from an original sin, a contradiction that the President is unwilling (or incapable) of seeing. The yellow vest protest originates from the gas price increase, that affected rural households and farmers in particular? But the malaise has much deeper roots, that are widespread. The French economy feels, after ten years, the full weight of a crisis that has hit very hard the middle and lower classes: Unemployment that fell too slowly (costing re-election to François Hollande ; austerity that, although less marked than in the peripheral eurozone countries, has reduced the perimeter and coverage of public services and of the welfare system, while increasing the tax burden; and, finally, the reduction of family allocations and welfare in general, which particularly affected the most disadvantaged categories. All of this led to what Julia Cagé, on French daily Le Monde, called “the purchasing power crisis”, that simmered for a long time, before exploding in the past weeks.

Emmanuel Macron has an enormous responsibility for the bursting of the crisis. True, the increase in the tax burden for the middle class is mainly due to François Hollande (under the impulse of an ambitious undersecretary, and then minister of the economy, named … Emmanuel Macron). One might even argue that the budget law for 2019 reverses the trend as that the reduction of some taxes (in particular the elimination of the housing tax for the majority of households, and the flat tax on capital income) has more than offset the reduction in social benefits.

What explains then the fact that the discontent emerges, so violently, just now? The explanation is simple: it is to be found in the approach that the French President pursued since he beginning of his mandate. Like Donald Trump, with whom he disagrees on almost everything, Emmanuel Macron believes in the so-called “trickle down” theory: shifting the tax burden away from the rich is the best strategy to revive growth, because these people are more productive than the average, and invest the extra income in innovative activities. The fruits of higher growth would then percolate to everyone, even those who were initially penalized by the tax reform. From the beginning of his mandate, Macron’s choice to give France a pro-business image was clear, leading to a drastic reduction of taxes on the richest, and making the taxation, for the upper part of the distribution, fundamentally regressive.

The last budget law represents the clearest proof of this approach. The “Institute for Public Policies” has shown (see the figure, taken from a Le Monde article appeared last October) that while the overall disposable income slightly increases, the bottom 20% and the upper-middle class see a substantial worsening of their situation, while the very rich (the top 1%) see their purchasing power increase of 6%.

The problem is, as an increasing body of evidence shows, that trickle down does not work. Favoring the richest does not increase productive investment (it rather tends to boost non-produced asset prices and unproductive consumption), and the impact on growth is both negligible and not shared; these days’ demonstrations stand to prove it. History cannot be rewritten, but the attempt to twist the tax system in favor of the ecological transition would probably have been met with much more enthusiasm, in a country like France where environmental awareness is high, where it not accompanied by the sentiment of increasing social injustice that Macron’s economic policies have deepened.

It is interesting to notice, in this regard, that traditional media have given a somewhat distorted image of the protest movement (which is very hard to clearly decrypt). A group of researchers from Toulouse University uses lexicographic analysis to show that the narrative of traditional media was centered on revolt against taxes (ras-le-bol fiscal), and therefore in contradiction with the request of better public services; this does not correspond to the message coming from social networks that organized “from the bottom” the movement, in which instead the predominant mood was revolt against social injustice and against the elites that grow richer and richer, while leaving the check for the others to pay. To sum up, a plea for a more equal and cohesive society.

How will this end? It is hard to say. The yellow vests have obtained a partial win, with the freezing of the gas increase, and with the measures announced by Macron on Monday. But it is unlikely that we will see a substantive change of economic policy, precisely because of the President’s views outlined above. He rushed to rule out any reinstatement of the wealth tax, because “in the past unemployment increased even when the wealth tax existed” (a rather unconvincing argument, to say the truth).

If higher incomes are not called to contribute to the effort (towards ecological transition, but more generally towards the financing of the French social model), even the measures just announced will have a very limited impact. The State will somehow have to take back with one hand (for example by reducing public services, that benefit lower income most, or increasing other taxes) what it just handed out with the other hand. The demand for social justice that confusedly emerges from the yellow vests movement will once more go unanswered, leaving untouched the tension that is ripping the French (and not just the French) society.

To meet these needs, a new political proposal would have to put the complex theme of the redistribution of resources in a globalized world at the center of its project. It would be necessary to rediscover the “Regulatory State” which, in the golden years of social democracy (and of the social right), guaranteed social and macroeconomic stability, and thus laid the foundations for investment, innovation, and growth. That role is more difficult to define in a globalized world in which individual States have limited room for maneuver, and in which therefore international cooperation, however difficult, is now the only way forward. But this challenge can not be avoided if we do not want movements such as those of yellow vests to fall prey to nativist autocratic populism.

(This is the translation of a piece I published in Italian on the Luiss Open website)

Trump and Reagan

A couple of days ago I had an interesting debate hosted by France 24, on Trumponomics. Interesting because there was an overall agreement between me and Dan Mitchell from Cato Institute, even if from totally opposite points of view, on the fact that Trumponomics does not exist. The Donald is pushing forward a number of inconsistent measures, whose final effect is impossible to forecast (except that it is a safe bet to say that it will not end well).

Mitchell argued of course that the only good policies imply the downsizing of the government. As one can easily imagine I would tend to disagree. And over and over again, during the 40 or so minutes of discussion, came back the reference to the golden era of Ronald Reagan. Trump needs to cut taxes, as Reagan did, and downsize government, as Reagan did. And growth and unemployment will return, as under Reagan

When I said that the problem of the US was not the lack of jobs per se, but rather the increasingly unequal distribution of income, that started precisely under Reagan, Mitchell replied that this was false (I officially spread fake truths!), claiming that median income under Reagan increased. Well, think again. An old post by Paul Krugman had already dispelled the mith, and I had written on it myself. I copy the figure from that post (updated) here:

So, while it is true that median income increased under Reagan-Bush (Mitchell is formally right), it is hard to define it an era or decreasing inequality I My conclusion back then was that growth does not lift all boats, and trickle-down economics does not exist. And Reagan did not do that well in terms of growth either. And did I mention twin deficits?

Just a final remark. The downsizing of government under Reagan is also a myth (which is rather good news, by the way): Look at OECD data:

I rest my case. People at Cato should pick their role models more carefully.

A Piketty Moment

Update (10/27): Comments rightly pointed to different deflators for the two series. I added a figure to account for this (thanks!)

Via Mark Thoma I read an interesting Atalanta Fed Comment about their wage tracker, asking whether the recent pickup of wages in the US is robust or not.

The first thing that came to my mind is that we’d need a robust and sustained increase, in order to make up for lost ground, so I looked for longer time series in Fred, and here is what I got

This yet another (and hardly original) proof of the regime change that occurred in the 1970s, well documented by Piketty. Before then, US productivity (output per hour) and compensation per hour roughly grew together. Since the 1970s, the picture is brutally different, and widely discussed by people who are orders of magnitude more competent than me.

[Part added 10/27: Following comments to the original post, I added real compensation defled with the GDP deflator. While this does not account for purchasing power changes, it is more directly comparable with real output. Here is the result:

The commentators were right, the divergence starts somewhat later, in the early 1980s. This makes it less of a Piketty moment, while leaving the broad picture unchanged.]

Next, I tried to ask whether it is better for wage earners, in this generally gloomy picture, to be in a recession or in a boom. I computed the difference between productivity (output per hour) and wages (compensation per hour), and averaged it for NBER recession and expansion periods (subperiods are totally arbitrary. i wanted the last boom and bust to be in a single row). Here is the table:

| Yearly Average Difference Between Changes in Productivity and in Wages | ||||

|---|---|---|---|---|

| In Recessions | In Expansions | Overall | % of Quarters in Recession | |

| 1947-2016 | 1.51% | 0.40% | 0.57% | 15% |

| 1947-1970 | 1.62% | -0.14% | 0.19% | 19% |

| 1970-2016 | 1.42% | 0.67% | 0.76% | 13% |

| 1980-1992 | 0.64% | 0.84% | 0.81% | 17% |

| 1993-2000 | N/A | 0.68% | 0.68% | 0% |

| 2001-2008Q1 | 4.07% | 1.10% | 1.41% | 10% |

| 2008Q2-2016Q2 | 2.17% | 0.12% | 0.49% | 18% |

| Source: Fred (my calculations) | ||||

| Compensation: Nonfarm Business Sector, Real Compensation Per Hour | ||||

| Productivity: Nonfarm Business Sector, Real Output Per Hour | ||||

No surprise, once again, and nothing that was not said before. The economy grows, wage earners gain less than others; the economy slumps, wage earners lose more than others. As I said a while ago, regardless of the weather stones keep raining. And it rained particularly hard in the 2000s. No surprise that inequality became an issue at the outset of the crisis…

There is nevertheless a difference between recessions and expansions, as the spread with productivity growth seems larger in the former. So in some sense, the tide lifts all boats. It is just that some are lifted more than others.

Ah, of course Real Compensation Per Hour embeds all wages, including bonuses and stuff. Here is a comparison between median wage,compensation per hour, and productivity, going as far back as data allow.

I don’t think this needs any comment.

The Blanchard Touch

Yesterday I commented on the intriguing box in which the IMF staff challenges one of the tenets of the Washington consensus, the link between labour market reform and economic performance.

But the IMF is not new to these reassessments. In fact over the past three years research coming from the fund has increasingly challenged the orthodoxy that still shapes European policy making:

- First, there was the widely discussed mea culpa in the October 2012 World Economic Outlook, when the IMF staff basically disavowed their own previous estimates of the size of multipliers, and in doing so they certified that austerity could not, and would not work (of course this led EU leaders to immediately rush to do more of the same).

- Then, the Fund tackled the issue of income inequality, and broke another taboo, i.e. the dichotomy between fairness and efficiency. Turns out that unequal societies tend to perform less well, and IMF staff research reached the same conclusion. And once the gates opened, it did not stop. The paper by Berg and Ostry was widely read. Then we had Ball et al on the distributional effects of fiscal consolidation (surprise, it increases inequality). Another paper investigated the channels for this link, highlighting how consolidation leads to increased inequality mostly via unemployment. And just last week I assisted to a presentation by IMF economists showing how austerity and inequality are positively related with political instability.

- On labour markets, before yesterday’s box 3.5, the Fund had disseminated research linking increased inequality with the decline in unionization.

- Then, of course, the “public Investment is a free lunch” chapter three of the World Economic Outlook, in the fall 2014.

- In between, they demolished another building block of the Washington Consensus: free capital movements may sometimes be destabilizing…

These results are not surprising per se. All of these issues are highly controversial, so it is obvious that research does not find unequivocal support for a particular view. All the more so if that view, like the Washington Consensus, is pretty much an ideological construction. Yet, the fact that research coming from the center of the empire acknowledges that the world is complex, and interactions among agents goes well beyond the working of efficient markets, is in my opinion quite something.

What does this mass (yes, now it can be called a mass) of work tells us? Three things, I would say. First, fiscal policy is back. it really is. The Washington Consensus does not exist anymore, at least in Washington. Be it because the multipliers are large, or because it has an impact on income distribution (and on economic efficiency); or again because public investment boosts growth, fiscal policy has a role to play both in dampening business cycle fluctuations and in facilitating stable and balanced long term growth. The fact that a large institution like the IMF has lent its support to this revival of consideration for fiscal policy, makes me hope that discussions about macroeconomic policy will be less ideological, even once the crisis will have passed.

The second thing I learn is that the IMF research department proves to be populated of true researchers, who continuously challenge and test their own views, and are not afraid of u-turns if their own research dictates them. I am sure it has always been the case. What is different from the past is that now they have a chief economist who seems more interested in understanding where the world goes than in preaching a doctrine.

The third remark is more problematic. If I write a paper saying that austerity will not be costly because multipliers are 0.5, and 2 years later retract my previous statement and argue that austerity is in fact self defeating, the impact on the world is zero. If the IMF does the same, during the two years huge suffering will be needlessly inflicted to masses of people. This poses a problem, as research by definition may be falsified. In the past an institution like the IMF would never have admitted a mistake. And we certainly do not want to go back there. Today they do admit the mistakes, but the suffering remains. The only way out to this problem is that the “new” IMF should learn to be cautious in its policy prescriptions, and always remember that any policy recommendation is bound to be sooner or later proven inappropriate by new data and research. We don’t live in a black and white world. Adopting a more prudent stance in dictating policies would be wise (in Brussels as well, it goes without saying). And of course, the disconnect between the army and the general is also a problem.

Raise Fed Rates Now?

A quick note on the US and the Fed. Pressure for rate rises never really stopped, but lately it has intensified. Today I read on the FT that James Bullard, Saint Louis Fed head, urges Janet Yellen to raise rates as soon as possible, to avoid “devastating asset bubbles”. Just a few months ago we learned that QE was dangerous because, once again through asset price inflation, it led to increasing inequality. Not to mention the inflationistas (thanks PK for the great name!) who since 2009 have been predicting Weimar-type inflation because of irresponsible Fed behaviour (a very similar pattern can be found in the EMU). Let’s play the game, for the sake of argument. After all, asset price inflation, and distortions in general are not unlikely in the current environment. So let’s assume that the Fed suddenly were convinced by its critics, and turned its policy stance to restrictive (hopefully this is just a thought experiment). I have two related questions to rate-raisers (the same two questions apply to QE opponents in the EMU):

- Do they think that private expenditure is healthy enough to grow and to sustain economic activity without the oxygen tent of monetary policy?

- If not, would they be willing to accept that monetary restriction is accompanied by a fiscal expansion?

I am afraid we all know the answer, at least to the second of these questions. Just yesterday, on Italian daily Il Corriere della Sera, Alberto Alesina and Francesco Giavazzi called for public expenditure cuts, invoking the confidence fairy and expansionary austerity (yes, you have read well. Check for yourself if you understand Italian. And check the date, it is 2015, not 2007) What Fed (and ECB) bashers tend to forget, in conclusion, is that central bankers are at the center of the stage, reluctantly, because they have to fill the void left, for different reasons, by fiscal policy. Look at the fiscal stance for the US:  Fiscal impulse, the discretionary stance of the US government, was positive only in 2008-2009, and has been restrictive since then. In other words, while the US were experiencing the worse crisis since the 1930s, while recovery was sluggish and jobless, the US government was pushing the brake. We all know why: political blockage and systematic boycott, by one side of Congress, of each and every one of the measures proposed by the administration (that was a bit too timid, if I may say so). Whatever the reasons, the fact remains that fiscal policy was of very limited help during the crisis. What do Fed bashers have to say about this? What would have happened if, faced with procyclical fiscal policy, the Fed had not stepped in with QE? I am afraid their answer would once again turn around confidence fairies… The EMU is pretty much in the same situation. The following figure shows the cumulative fiscal impulse since 2008 for a number of countries:

Fiscal impulse, the discretionary stance of the US government, was positive only in 2008-2009, and has been restrictive since then. In other words, while the US were experiencing the worse crisis since the 1930s, while recovery was sluggish and jobless, the US government was pushing the brake. We all know why: political blockage and systematic boycott, by one side of Congress, of each and every one of the measures proposed by the administration (that was a bit too timid, if I may say so). Whatever the reasons, the fact remains that fiscal policy was of very limited help during the crisis. What do Fed bashers have to say about this? What would have happened if, faced with procyclical fiscal policy, the Fed had not stepped in with QE? I am afraid their answer would once again turn around confidence fairies… The EMU is pretty much in the same situation. The following figure shows the cumulative fiscal impulse since 2008 for a number of countries:  The figure speaks for itself. With the exception of Japan (thanks Abenomics!) governments overall acted as brakes for the economy (Alesina and Giavazzi should look at the data for Italy, by the way). Central banks had to act in the thunderous silence of fiscal policy. So I repeat my question once again: who would be willing to exchange a normalization of monetary policy with a radical change in the fiscal stance? To conclude, yes, monetary policy has been very proactive (even Mario Draghi’s ECB); yes, this led us in unchartered lands, and we do not fully grasp what will be the long term effects of QEs and unconventional monetary policies; yes, some distortions are potentially dangerous. But central bankers had no choice. We are in a liquidity trap, and the main tool to be used should be fiscal policy. Monetary policy could and should be normalized, if only fiscal policy would finally take the witness, and the burden to lift the economy out of its woes; if fiscal policy finally tackled the increasing inequality that is choking the economy. If fiscal policy did its job, in other words.

The figure speaks for itself. With the exception of Japan (thanks Abenomics!) governments overall acted as brakes for the economy (Alesina and Giavazzi should look at the data for Italy, by the way). Central banks had to act in the thunderous silence of fiscal policy. So I repeat my question once again: who would be willing to exchange a normalization of monetary policy with a radical change in the fiscal stance? To conclude, yes, monetary policy has been very proactive (even Mario Draghi’s ECB); yes, this led us in unchartered lands, and we do not fully grasp what will be the long term effects of QEs and unconventional monetary policies; yes, some distortions are potentially dangerous. But central bankers had no choice. We are in a liquidity trap, and the main tool to be used should be fiscal policy. Monetary policy could and should be normalized, if only fiscal policy would finally take the witness, and the burden to lift the economy out of its woes; if fiscal policy finally tackled the increasing inequality that is choking the economy. If fiscal policy did its job, in other words.

I don’t know why, but I have the feeling that Janet Yellen and Mario Draghi would not completely disagree.

Marginal Productivity? Think Again

I am writing a paper on inequality and the crisis, for which I used Piketty and Saez ‘s World Top Income Database to try to understand whether the distributional effect changed over time. Unfortunately their data cover 2012 only for a handful of countries, among which are the United States; waiting for new data here is the evolution of income percentiles, including capital gains, from 2007 to 2009 (yellow bars), and from 2009 to 2012 (red bars):

The financial crisis of 2007-2008 mainly hit asset prices, thus having a major impact on the richest layers of the income distribution. In fact, the top 0.1% to 0.01% (a handful of people) lost more than 40% of their income in real terms, while average income of the bottom 90% dropped of around 10%. This was short-lasted, nevertheless, as the prolonged recession, and the jobless recovery that followed, quickly restored, and further deepened the distance between the rich on one side and the middle and lower classes on the other. Since 2009 average income of the bottom 95% stagnated (for the bottom 90% it kept decreasing). Nothing really new, here. The iAGS 2014 report, to which I (marginally) contributed, reaches similar conclusions. But I thought it would be interesting to share it.

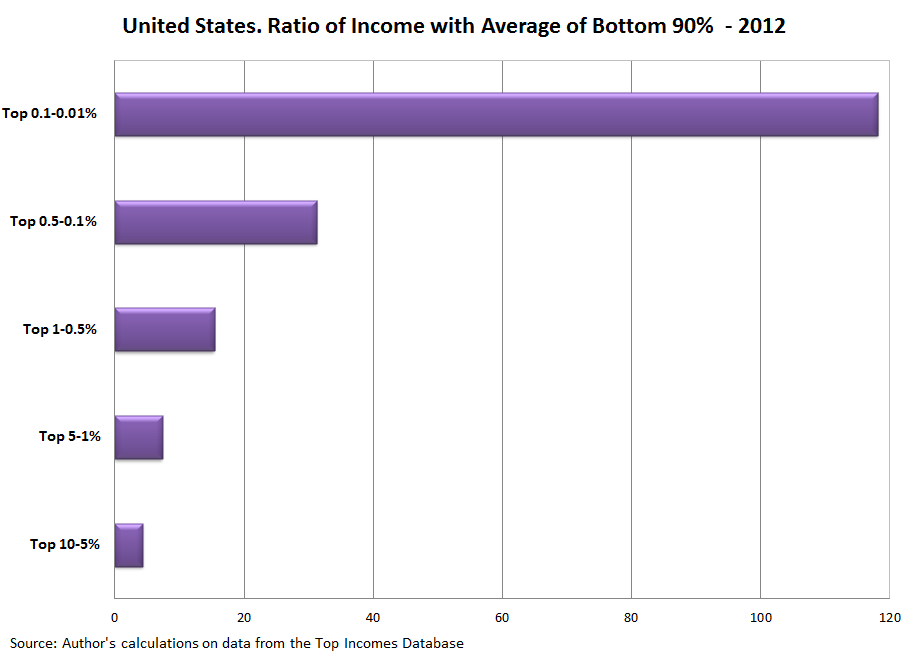

And while we are at it, here are the ratios of average income of those at the very top, with respect to income of the bottom 90% (from the same dataset):

The top 0.1%-0.01%, the same handful of people as before, has an average income that is 120 times the average income of the bottom 90%. This is also barely breaking news…

Now, as we all know, the traditional view on income distribution states that factors of production are paid according to their contribution to the production process (their “marginal productivity”). Within this traditional view, the recent steep increase of inequality would be explained by skill-biased technical progress and increased competition in the globalized labor market: the entrance in the global labor market of low-skilled workers from emerging and developing economies lowered the average marginal productivity of labor, thus reducing its share of national income. Increasing inequality would then be an ineluctable process that policy is not supposed to address, if not at the price of reduced efficiency and growth. Is this a caricature? Not so much. in his recent Project Syndicate comment on Piketty, Kenneth Rogoff proposes once again the old tradeoff between inequality and growth that the crisis seemed to have buried once and for all (just look at the widely cited IMF discussion paper by Ostry et al). The traditional view is alive and kicking, and those who oppose it are dangerous liberal extremists! After all, Rogoff tells us, the tide raises all boats…

The bottom line is that if a top executive makes on average 120 times the wage of his or her employee, well, this means that he or she is 120 times more productive. Rent seeking and political capture play no role in explaining the difference in pay. Circulez, il n’y a rien à voir…

Nothing new under the sky, I guess. But it is important, from time to time, to send out reminders.

Overheat to Raise Potential Growth?

Update, March 20th: Speaking of ideological biases concerning inflation, Paul Krugman nails it, as usual.

On today’s Financial Times, Phillip Hildebrand gives yet another proof of unwarranted inflation terror. His argument is not new: In spite of the consensus on a weak recovery, the US economy may be close to its potential , so that further monetary stimulus would eventually be inflationary.

He then deflects (?) the objection that decreasing unemployment reflects decreasing labour force participation rather than new employment, by suggesting that it is hard to know how many of the 13 millions jobs missing are structural, i.e.not linked to the crisis. I think it is worth quoting him, because otherwise it would be hard to believe:

However, an increasingly vocal group of observers, including within the Fed, posits that more of the fall in the participation rate appears to have been structural than cyclical, and it was even predictable – the result of factors such as an ageing workforce and the effect of technology on jobs.

(the emphasis is mine). Now look at this figure, quickly produced from FRED data: Read more

Reduce Inequality to Fight Secular Stagnation

Larry Summers’ IMF speech on secular stagnation partially shifted the attention from the crisis to the long run challenges facing advanced economies. I like to think of Summers’ point of as a conjectures that “in the long run we are all Keynesians”, as we face a permanent shortage of demand that may lead to a new normal made of hard choices between an unstable, debt-driven growth, and a quasi-depressed economy. A number of factors, from aging and demographics to slowing technical progress, may support the conjecture that globally we may be facing permanently higher levels of savings and lower levels of investment, leading to negative natural rates of interest. Surprisingly, another factor that had a major impact in the long-run compression of aggregate demand has been so far neglected: the steep and widespread increase of inequality. Reversing the trend towards increasing inequality would then become a crucial element in trying to escape secular stagnation.

Read More

The Italian Job

A follow-up of the post on public investment. I had said that the resources available based on my calculation were to be seen as an upper bound, being among other things based on the Spring forecasts of the Commission (most likely too optimistic).

And here we are. On Friday the IMF published the result of its Article IV consultation with Italy, where growth for 2013 is revised downwards from -1.3% to -1.8%.

In terms of public finances, a crude back-of-the-envelop estimation yields a worsening of deficit of 0.25% (the elasticity is roughly 0.5). This means that in the calculation I made based on the Commission’s numbers, the 4.8 billions available for 2013 shrink to 1.5 once we take in the IMF numbers. It is worth reminding that besides Germany, Italy is the only large country who can could benefit of the Commission’s new stance.

And while we are at Italy, the table at page 63 of the EC Spring Forecasts (pdf) is striking. The comparison of 2012 with the annus horribilis 2009 shows that private demand is the real Italian problem. The contribution to growth of domestic demand was of -3.2% in 2009, and -4.7% in 2012! In part this is because of the reversed fiscal stimulus; but mostly because of the collapse of consumption (-4.2% in 2012, against -1.6% in 2009). Luckily, the rest of the world is recovering, and the contribution of net exports, went from -1.1% in 2009 to 3.0% in 2012. This explains the difference in GDP growth between the -5.5% of 2009 and the -2.4% of 2012.

Italian households feel crisis fatigue, and having depleted their buffers, they are today reducing consumption. I remain convinced that strong income redistribution is the only quick way to restart consumption. Looking at the issues currently debated in Italy, this could be attempted reshaping both VAT and property taxes so as to impact the rich and the very rich significantly more than the middle classes. The property tax base should be widened to include much more than just real estate, and an exemption should be introduced (currently in France it is 1.2 millions euro per household). Concerning VAT, a reduction of basic rates should be compensated by a significant increase in rates on luxury goods.

Chances that this will happen?

Keynes Blog

Keynes Blog

- Più SURE, meno MES

- Come Mario Draghi ha salvato l’euro

- Le conseguenze economiche della pandemia: Mario Draghi e le scelte di politica economica ai tempi del coronavirus

- A lezione da Keynes, ripensando la macroeconomia. Recensione de “La scienza inutile” di F. Saraceno

- L’euro è una cosa troppo seria per lasciarla in mano ai soliti europeisti (e ai noeuro)

- Squilibri nell’eurozona: non è un problema di competitività di prezzo

- Intervista a Francesco Saraceno: “Sta cambiando la narrativa dell’economia ma non nella politica europea”

- Un nuovo errore di Blanchard sulla Grecia?

- La “germanizzazione” dell’Eurozona

- La politica monetaria della BCE: una sola misura non va bene per nessuno