Archive

Marginal Productivity? Think Again

I am writing a paper on inequality and the crisis, for which I used Piketty and Saez ‘s World Top Income Database to try to understand whether the distributional effect changed over time. Unfortunately their data cover 2012 only for a handful of countries, among which are the United States; waiting for new data here is the evolution of income percentiles, including capital gains, from 2007 to 2009 (yellow bars), and from 2009 to 2012 (red bars):

The financial crisis of 2007-2008 mainly hit asset prices, thus having a major impact on the richest layers of the income distribution. In fact, the top 0.1% to 0.01% (a handful of people) lost more than 40% of their income in real terms, while average income of the bottom 90% dropped of around 10%. This was short-lasted, nevertheless, as the prolonged recession, and the jobless recovery that followed, quickly restored, and further deepened the distance between the rich on one side and the middle and lower classes on the other. Since 2009 average income of the bottom 95% stagnated (for the bottom 90% it kept decreasing). Nothing really new, here. The iAGS 2014 report, to which I (marginally) contributed, reaches similar conclusions. But I thought it would be interesting to share it.

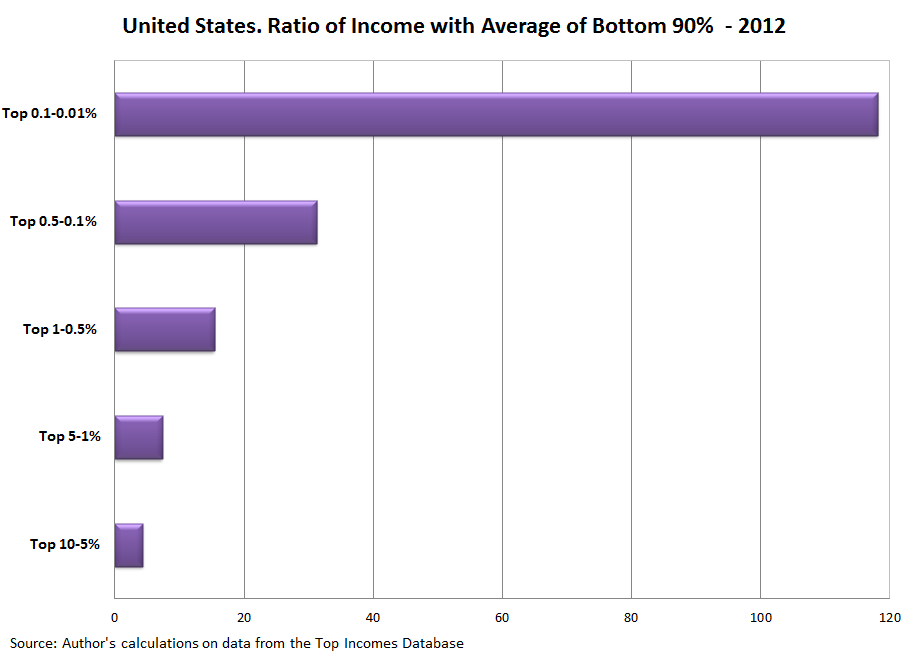

And while we are at it, here are the ratios of average income of those at the very top, with respect to income of the bottom 90% (from the same dataset):

The top 0.1%-0.01%, the same handful of people as before, has an average income that is 120 times the average income of the bottom 90%. This is also barely breaking news…

Now, as we all know, the traditional view on income distribution states that factors of production are paid according to their contribution to the production process (their “marginal productivity”). Within this traditional view, the recent steep increase of inequality would be explained by skill-biased technical progress and increased competition in the globalized labor market: the entrance in the global labor market of low-skilled workers from emerging and developing economies lowered the average marginal productivity of labor, thus reducing its share of national income. Increasing inequality would then be an ineluctable process that policy is not supposed to address, if not at the price of reduced efficiency and growth. Is this a caricature? Not so much. in his recent Project Syndicate comment on Piketty, Kenneth Rogoff proposes once again the old tradeoff between inequality and growth that the crisis seemed to have buried once and for all (just look at the widely cited IMF discussion paper by Ostry et al). The traditional view is alive and kicking, and those who oppose it are dangerous liberal extremists! After all, Rogoff tells us, the tide raises all boats…

The bottom line is that if a top executive makes on average 120 times the wage of his or her employee, well, this means that he or she is 120 times more productive. Rent seeking and political capture play no role in explaining the difference in pay. Circulez, il n’y a rien à voir…

Nothing new under the sky, I guess. But it is important, from time to time, to send out reminders.

Countercyclical no More

Browsing national accounts may be an inexhaustible source of insight on the current debate about austerity. Take this figure, which shows the evolution of real GDP and of its components for the US and the EMU, making the first quarter of 2008 equal to 100.

I tracked in particular the evolution of private (consumption plus investment) and public expenditure on good and services.

Of Old Ideas about Inequality and Growth

Update: An edited version of this piece appeared as a Project Syndicate commentary

A few weeks ago on Project Syndicate Raghuram Rajan offered his view on inequality and growth, thought provoking as usual. His argument can be summarized as follows:

- Inequality increased starting from the 1970s, across the board

- Two different explanations of this increase can be offered: a progressive one, that blames pro-rich policies, and an “alternative” one, that focuses on skill biased technical progress. I do not understand Rajan’s restraint, and as I like symmetry, I will label this alternative view “conservative”.

- Both views agree that inequality led to excessive debt and hence to the crisis.

- According to Rajan, nevertheless, the alternative/conservative view is more apt at explaining what happened to Europe, that remained more egalitarian, but was able to hide the ensuing low growth and competitiveness through the euro and increased debt.

- The exception is Germany where, following the reunification, structural reforms had to be implemented to reduce workers’ protection. This explains why Germany today is so strong in Europe.

- Thus the solution is for Southern Europe to implement structural reforms and accept increased inequality through lower workers’ protection; the alternative is sliding into an “egalitarian decline” like Japan.

The way I see it, there are a number of problems with Rajan’s analysis, and more importantly a fundamental (and unproven) assumption that underlies his argument. Let me start with the problems in his analysis, and then I’ll turn to the core of this piece, i.e. challenging the underlying assumption.

And I Thought I was the Gloomy Economist…

Give a look at Dani Rodrick on Project Syndicate (in a number of languages). The scary thing is that it is not completely implausible…

Inequality and Global Imbalances

European institutions and policy makers seem to share a narrative of the crisis essentially centered on sovereign debt, which they consider as the sole obstacle to a return to a normal state of affairs. Yet, it suffices to look at the other side of the Atlantic, or to go back to the events of 2008, to question this narrative. With the exception of Greece (whose GDP represents 2.5% of that of the eurozone), sovereign debt is today more a consequence than a cause of the crisis. This does not imply that it should be the object of a benign neglect; but understanding why we came to a systemic crisis of this magnitude is crucial for having a coherent discussion of future perspectives.

Keynes Blog

Keynes Blog

- Più SURE, meno MES

- Come Mario Draghi ha salvato l’euro

- Le conseguenze economiche della pandemia: Mario Draghi e le scelte di politica economica ai tempi del coronavirus

- A lezione da Keynes, ripensando la macroeconomia. Recensione de “La scienza inutile” di F. Saraceno

- L’euro è una cosa troppo seria per lasciarla in mano ai soliti europeisti (e ai noeuro)

- Squilibri nell’eurozona: non è un problema di competitività di prezzo

- Intervista a Francesco Saraceno: “Sta cambiando la narrativa dell’economia ma non nella politica europea”

- Un nuovo errore di Blanchard sulla Grecia?

- La “germanizzazione” dell’Eurozona

- La politica monetaria della BCE: una sola misura non va bene per nessuno