Archive

Blame the World?

Yesterday’s headlines were all for Germany’s poor performance in the second quarter of 2014 (GDP shrank of 0.2%, worse than expected). That was certainly bad news, even if in my opinion the real bad news are hidden in the latest ECB bulletin, also released yesterday (but this will be the subject of another post).

Not surprisingly, the German slowdown stirred heated discussion. In particular Sigmar Gabriel, Germany’s vice-chancellor, blamed the slowdown on geopolitical risks in eastern Europe and the Near East. Maybe he meant to be reassuring, but in fact his statement should make us all worry even more. Let me quote myself (ach!), from last November:

Even abstracting from the harmful effects of austerity (more here), the German model cannot work for two reasons: The first is the many times recalled fallacy of composition): Not everybody can export at the same time. The second, more political, is that by betting on an export-led growth model Germany and Europe will be forced to rely on somebody else’s growth to ensure their prosperity. It is now U.S. imports; it may be China’s tomorrow, and who know who the day after tomorrow. This is of course a source of economic fragility, but also of irrelevance on the political arena, where influence goes hand in hand with economic power. Choosing the German economic model Europe would condemn itself to a secondary role.

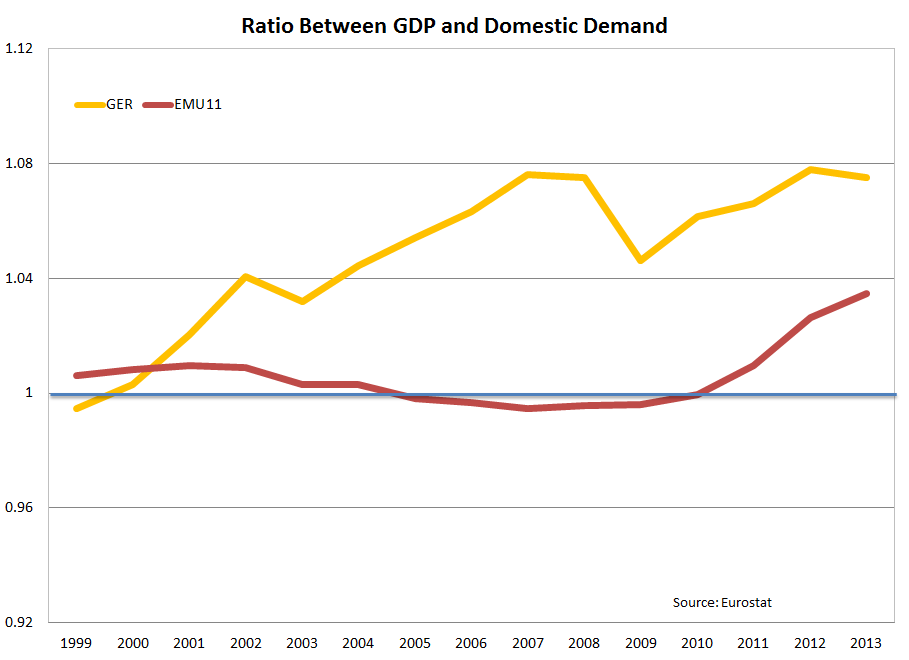

I have emphasized the point I want to stress, once again, here: adopting an export-led model structurally weakens a country, that becomes unable to find, domestically, the resources for sustainable and robust growth. And here we are, the rest of the world sneezes, and Germany catches a cold. The problem is that we are catching it together with Germany:

The ratio of German GDP over domestic demand has been growing steadily since 1999 (only in 19 quarters out of 72, barely a third, domestic demand grew faster than GDP). And what is more bothersome is that since 2010 the same model has been adopted by imposed to the rest of the eurozone. The red line shows the same ratio for the remaining 11 original members of the EMU, that was at around one for most of the period, and turned frankly positive with the crisis and implementation of austerity.It is the Berlin View at work, brilliantly and scaringly exposed by Bundesbank President Jens Weidmann just a couple of days ago. We are therefore increasingly dependent on the rest of the world for our (scarce) growth (the difference between the ratio and 1 is the current account balance).

It is easy today to blame Putin, or China, or tapering, or alien invasions, for our woes. Easy but wrong. Our pain is self-inflicted. Time to change.

ECB: One Size Fits None

Eurostat just released its flash estimate for inflation in the Eurozone: 0.5% headline, and 0.8% core. We now await comments from ECB officials, ahead of next Thursday’s meeting, saying that everything is under control.

Just this morning, Wolfgang Münchau in the Financial Times rightly said that EU central bankers should talk less and act more. Münchau also argues that quantitative easing is the only option. A bold one, I would add in light of todays’ deflation inflation data. Just a few months ago, in September 2013, Bruegel estimated the ECB interest rate to be broadly in line with Eurozone average macroeconomic conditions (though, interestingly, they also highlighted that it was unfit to most countries taken individually).

In just a few months, things changed drastically. While unemployment remained more or less constant since last July, inflation kept decelerating until today’s very worrisome levels. I very quickly extended the Bruegel exercise to encompass the latest data (they stopped at July 2013). I computed the target rate as they do as

(if you don’t like the choice of parameters, go ask the Bruegel guys. I have no problem with these). The computation gives the following:

Using headline inflation, as the ECB often claims to be doing, would of course give even lower target rates. As official data on unemployment stop at January 2014, the two last points are computed with alternative hypotheses of unemployment: either at its January rate (12.6%) or at the average 2013 rate (12%). But these are just details…

So, in addition to being unfit for individual countries, the ECB stance is now unfit to the Eurozone as a whole. And of course, a negative target rate can only mean, as Münchau forcefully argues, that the ECB needs to get its act together and put together a credible and significant quantitative easing program.

Two more remarks:

- A minor one (back of the envelope) remark is that given a core inflation level of 0.8%, the current ECB rate of 0.25%, is compatible with an unemployment gap of 1.95%. Meaning that the current ECB rate would be appropriate if natural/structural unemployment was 10.65% (for the calculation above I took the value of 9.1% from the OECD), or if current unemployment was 11.5%.

- The second, somewhat related but more important to my sense, is that it is hard to accept as “natural” an unemployment rate of 9-10%. If the target unemployment rate were at 6-7%, everything we read and discuss on the ECB excessively restrictive stance would be significantly more appropriate. And if the problem is too low potential growth, well then let’s find a way to increase it…

What is Wrong with the EU?

Eurostat just released the 2012 figures for poverty and social exclusion in the EU. The numbers are terrifying. Let me quote the press release: “In 2012, 124.5 million people, or 24.8% of the population, in the EU were at risk of poverty or social exclusion, compared with 24.3% in 2011 and 23.7% in 2008. This means that they were in at least one of the following three conditions: at-risk-of-poverty, severely materially deprived or living in households with very low work intensity”

One may be tempted to shrug. After all, 1% in four years, is not that much. Let me put actual people behind the numbers: The number of people at risk of poverty increased of 5.5 millions between 2008 and 2012. Strikingly, always looking at Eurostat data, the number of jobs lost in the EU28 over the same period is almost exactly the same (-5.4 millions).

This is plain unacceptable. And teaches us two lessons

- Our welfare system is not capable anymore to shield workers from the hardship of business cycles. We progressively dismantled welfare, becoming “more like the United States”. But we stubbornly refuse to accept the consequence of this, i.e. that fiscal and monetary policy need (like in the US) to be proactive and flexible, so as to dampen the cycle. Constraints to macroeconomic policy, coupled with a diminished protection from the welfare state, spell disaster, social exclusion, and the destruction of the social fabric.

- The second lesson is that these numbers are there to stay. The economy may recover, but the loss of confidence, of capacity, of social status of those who we pushed into hardship, will stay with us for years to come. We are destroying human capital at amazing speed.

What is enraging is that none of this was inevitable. The crisis could have been shielded by less ideological leadership in European institutions and in some most European capitals. Frontloading of austerity in the periphery was a terrible mistake. Not accompanying it with fiscal expansion in the core was a crime, showing of how little solidarity counts, facing the protestant urge to “punish the sinners”.

The result is that one of the most affluent economic areas of the world barely notices that one quarter of its population lives at risk of poverty. What is wrong with us?

Raepetita Iuvant

Yesterday Eurostat published growth flash estimates for a number of EU countries. As expected, they do not look good. In 2013 Q1 the eurozone has lost 1 per cent of its GDP with respect to the first quarter of 2012 (-0.7 for the EU 27). It is the longest recession since the inception of the single currency, and it brings with it record unemployment at 12.1 per cent.

Not surprising, I said, because in spite of increasing talks about softened austerity, austerity ain’t over. In many countries, government final consumption in real terms (the G in national accounting equations, just to be clear) sharply decreased. And this is, surprise, correlated with subsequent growth:

Surprise! Spillovers Exist!

Eurostat GDP data are out. The eurozone is in recession, and it is worse than expected (-0.6% in 2012). Austerity is not working, and is recessionary. Wow, who would have said it…

Seriously, so long for the widespread optimism of a few weeks ago. The crisis is not over, we actually are in the middle of it. The way I see it, things will get worse before they get better (if they do get better).

Also interesting, Germany’s export-led growth strategy is panting. The fourth quarter of 2012 was rather bad (worse than in France, for example), and this is due to lower investment on one side, and to weaker trade (exports fell more than imports). Here is an excerpt of today’s press release of the German statistical office, Destatis:

In a quarter-on-quarter comparison (adjusted for price, seasonal and calendar variations), signals from the domestic territory were rather mixed according to provisional calculations: household and government final consumption expenditure went up slightly. In contrast, gross fixed capital formation in construction decreased a bit and gross fixed capital formation in machinery and equipment was down markedly on the third quarter of 2012. The decline of the gross domestic product at the end of 2012 was mainly due to the comparably weak German foreign trade: in the final quarter of 2012, exports of goods went down much more than imports of goods.

Germany stubbornly refuses to accommodate austerity in the periphery with a domestic impulsion. This makes adjustment for the rest more painful, and impacts expectations at home. This is why investment dropped significantly. My take on this is that if Germany had been only moderately more expansionist at home, expectations would not have been dashed (even if slightly increasing, in January the IFO index of German business confidence stagnates at around 104 at the moment, after hitting an all time high of 115.40 in February of 2011). And investment figures would be substantially better.

So, we learned today that austerity does indeed reduce growth, and that it spills to other countries. Two surprises in one day. It will need a hell of an effort to forget all of this before tomorrow!

Keynes Blog

Keynes Blog

- Più SURE, meno MES

- Come Mario Draghi ha salvato l’euro

- Le conseguenze economiche della pandemia: Mario Draghi e le scelte di politica economica ai tempi del coronavirus

- A lezione da Keynes, ripensando la macroeconomia. Recensione de “La scienza inutile” di F. Saraceno

- L’euro è una cosa troppo seria per lasciarla in mano ai soliti europeisti (e ai noeuro)

- Squilibri nell’eurozona: non è un problema di competitività di prezzo

- Intervista a Francesco Saraceno: “Sta cambiando la narrativa dell’economia ma non nella politica europea”

- Un nuovo errore di Blanchard sulla Grecia?

- La “germanizzazione” dell’Eurozona

- La politica monetaria della BCE: una sola misura non va bene per nessuno