Small Germany?

Today we learn from Daniel Gros, on Project Syndicate that the emphasis on German surplus is misplaced:

The discussion of the German surplus thus confuses the issues in two ways. First, though the German economy and its surplus loom large in the context of Europe, an adjustment by Germany alone would benefit the eurozone periphery rather little. Second, in the global context, adjustment by Germany alone would benefit many countries only a little, while other surplus countries would benefit disproportionally. Adjustment by all northern European countries would have double the impact of any expansion of demand by Germany alone, owing to the high degree of integration among the “Teutonic” countries.

Fascinating. The bulk of the argument is that Germany is a small player in the global economy, and therefore that its actions have no impact. I have two objections to Gros’ argument.

The first is trivially quantitative (and boring, I must admit). Gros claims that the German surplus is quantitatively small if related to world GDP, and even by looking at the Eurozone alone. He furthermore claims that a reduction of the German surplus would mostly benefit other exporter core countries (Finland, Austria, the Netherlands), and not the periphery. He relies on a figure: of one euro of increased imports by Germany, only 10 cents would go to exports of peripheral countries. Ok, let’s play the game. Gros does not give the sources of his data, so I took data from the OECD Economic Outlook. for 2013 the OECD projects the German current account surplus to be Euro 191bn. Assume that Germany were to reabsorb it playing equally on exports and imports. This would mean that a German rebalancing would yield increased exports of 50% of 191 bn, i.e. 95 bn. Taking Gros’ figure of 10% of it going to peripheral countries’ exports, this makes 9.5 billions. Irrelevant? Not sure. If we take the combined GDP of the strict periphery (still OECD data), namely Greece, Portugal, Ireland, Spain, 9.5 billions are 0.62% of GDP. Including Italy in the group, we are at 0.3%. Thus, if Germany had a balanced current account, this would give (slightly less or slightly more than) half a percentage point of GDP in increased exports for the periphery. Germany does not seem so small after all…

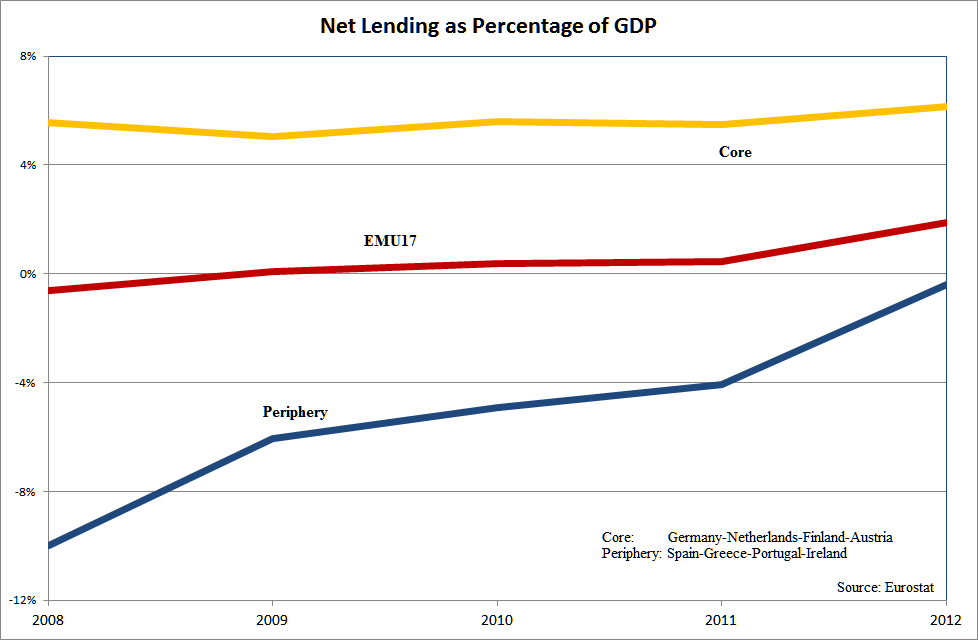

But I have a much more substantive objection, that in my opinion invalidates completely Gros’ defense of Germany. Gros neglects the macroeconomic impact of Germany’s management of the eurozone crisis, and of the overall restrictive stance that was imposed on the zone as a whole. Just give another look at the net lending figure I commented a while ago:

The Eurozone crisis management laid the burden of adjustment only on peripheral countries, with the result that the EMU as a whole has become a net saver, and siphons aggregate demand from the rest of the world (look also here and here. I have the feeling I barely discussed anything else, lately). Eurostat released today its estimates of current account balances for the Eurozone that, for 2013Q3 stand at 2.2% of GDP (52.6 billion euro). This is far from negligible, and is changing the balance between the Eurozone and the United States. Look at the following, also taken from OECD data:

The red bars represent the US current account deficit, that after a sharp reduction in the midst of the crisis, stabilized at around one hundred billions a year. The EMU balance (yellow bars) added to the total deficit in 2008, then was virtually zero in 2009-10, and since 2011 has grown to cover around half of the US deficit.

To sum up, we are quickly converging towards a well known pattern: the US excess savings is for a large part (the blue line) financed with excess savings from Europe. Before the crisis, during the peripheral spending binge, excess savings would essentially come from the core. Now, the Berlin View has transformed the whole Eurozone in net saver.

It is hard to believe, as Gros claims, that Germany is too small to alter this state of affairs. If the German government embarked in a serious effort of domestic demand expansion (private and public), and exerted a modicum of moral suasion on the smaller core creditor countries, the eurozone could at least stop subtracting aggregate demand from the rest of the world. And maybe, who knows, even one day contribute to global growth.

Share this:

Leave a comment

Keynes Blog

Keynes Blog

- Più SURE, meno MES

- Come Mario Draghi ha salvato l’euro

- Le conseguenze economiche della pandemia: Mario Draghi e le scelte di politica economica ai tempi del coronavirus

- A lezione da Keynes, ripensando la macroeconomia. Recensione de “La scienza inutile” di F. Saraceno

- L’euro è una cosa troppo seria per lasciarla in mano ai soliti europeisti (e ai noeuro)

- Squilibri nell’eurozona: non è un problema di competitività di prezzo

- Intervista a Francesco Saraceno: “Sta cambiando la narrativa dell’economia ma non nella politica europea”

- Un nuovo errore di Blanchard sulla Grecia?

- La “germanizzazione” dell’Eurozona

- La politica monetaria della BCE: una sola misura non va bene per nessuno

Your calculations of the impact of a German rebalancing on other EU members are way too small. A demand push would act mostly – not just 50% – through increased German imports, because there is still an output gap in Germany to be filled before prices rise: an income effect, not a substitution effect. But even if you assume that a demand push causes inflation in Germany – you get rebalancing through a substitution effect, so you get your 50% result: half rebalancing only materializes through higher German imports -, lowering German competitiveness and exports would cause import substitution and a domestic demand push elsewhere – in Italy Spain etc.

Then there are multiplier and spillover effects in europe.

Then there is an improvement of peripherical EU countries in world markets – for a given ECB monetary policy.

Finally, there would be an improvement in fiscal deficits in the south of europe that would reduce the need for austerity.

The impact of a German rebalancing on the GDP of Italy would be in the order of 2% (back of the envelope calculataions).

LikeLike

Nothing to object. I was being conservative!

LikeLike